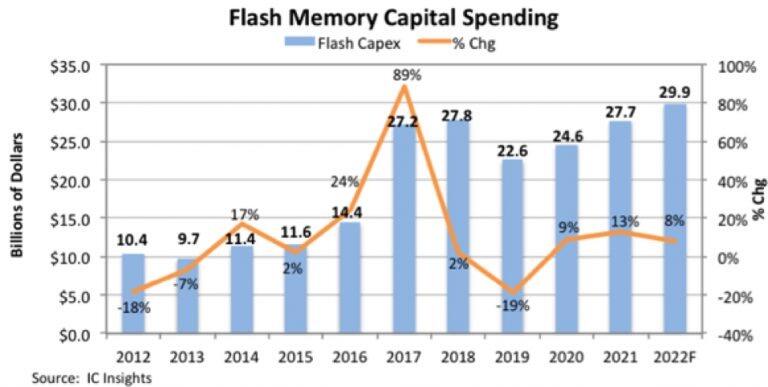

Foreign analysts IC Insights forecast that NAND flash CAPEX will grow 8% to $29.9 billion this year, surpassing $27.8 billion in 2018. flash CAPEX soared in 2017 when the industry made the transition to 3D NAND and has exceeded $20 billion each year since then. In 2022, flash memory CAPEX is expected to increase to $29.9 billion as both large and small suppliers maintain moderately aggressive spending levels.

The $29.9 billion in spending represents 16 percent of the overall IC industry’s projected capital spending of $190.4 billion in 2022, second only to the foundry segment, which is expected to account for 41 percent of industry capital spending this year.

Recent new upgrades to NAND flash fabs include Samsung’s Pyeongtaek 1 and 2 lines (also used for DRAM and foundry); Samsung’s Phase II investment in Xi’an, China; Armored Man’s Fab 6 and Fab K1 fabs in Iwate, Japan; and Micron’s third flash fab in Singapore. In addition, SK Hynix has equipped the remaining space in its M15 fab with NAND flash memory.

New fabs and equipment will be needed over the forecast period as NAND flash suppliers prepare to compete for capacity for 200+ layer flash chips from late 2022 through 2023. Samsung and Micron could be the first companies to start volume production of 200-layer NAND later this year. Both companies and SK Hynix are currently producing 176 layers of NAND in volume, and Samsung’s fab in Xi’an, China, is (or will become) a key manufacturing base for leading NAND with two fabs, each capable of producing 120,000 wafers per month when fully operational. With an increasing focus on enterprise storage applications, SK Hynix expects to migrate to 196 layers in 2023.

Related:

- 2025 Semiconductor Outlook: CapEx of Leading Chipmakers

- Semiconductor Market: Micron’s Product Prices Surge by 2025

- Tech Giants’ New Tactic: Flying Wafers to Skirt EUV Ban

- 300mm Wafer Fab Spending to Exceed $100 Billion in 2024!

Disclaimer:

- This channel does not make any representations or warranties regarding the availability, accuracy, timeliness, effectiveness, or completeness of any information posted. It hereby disclaims any liability or consequences arising from the use of the information.

- This channel is non-commercial and non-profit. The re-posted content does not signify endorsement of its views or responsibility for its authenticity. It does not intend to constitute any other guidance. This channel is not liable for any inaccuracies or errors in the re-posted or published information, directly or indirectly.

- Some data, materials, text, images, etc., used in this channel are sourced from the internet, and all reposts are duly credited to their sources. If you discover any work that infringes on your intellectual property rights or personal legal interests, please contact us, and we will promptly modify or remove it.