On March 27th, U.S. President Biden signed a presidential resolution authorizing the use of the Defense Production Act (DPA) to allocate $50 million (equivalent to approximately RMB 340 million) to support the U.S. printed circuit board (PCB) and advanced chip packaging industries. The aim of this move is to ensure that PCBs can be produced in the United States.

① Inconspicuous PCBs

PCB is an abbreviation for Printed Circuit Board, which is a circuit board that connects various points together with wires and solder pads. PCBs may not be conspicuous in the entire semiconductor industry chain, but they are widely used in electronic devices, including personal computers, communication base stations, mobile phones, household appliances, critical mission servers, and military equipment.

So why has the United States started to value PCBs?

This all started with the decline of American manufacturing. Labor costs in the United States have always been significantly higher than in other countries, but the productivity level in the United States has compensated for this difference. However, with the progress of globalization, many low-level and low-tech industries have started to shift to Asia, resulting in the loss of low-tech industries.

Coincidentally, the PCB industry is a labor-intensive industry that requires manual operation and assembly-line work with a large number of automated devices. A medium-sized PCB company can have several thousand employees.

Therefore, the history of PCB has also experienced a development change from “dominated by Europe and the United States” to “dominated by Asia.”

In 2000, over 70% of the world’s PCB output was distributed in the Americas, Europe, and Japan. From 2008 to 2016, the proportion of PCB output in the Americas, Europe, and Japan continued to decline globally, while the global share of PCB output in mainland China continued to increase from 31.18% in 2008 to 47.36%. Due to the relatively low labor costs, PCB has become an unstoppable trend in Asia, and the global PCB industry has gradually shifted its focus to Asia.

Today, Asia has undoubtedly become a gathering place for PCB development, forming a new pattern centered on Asia (especially mainland China) and supplemented by other regions.

According to a study conducted by Information in 2022, while the US only has five PCB manufacturers, China has the most with a total of 69 companies in the industry, followed by Taiwan (27), Japan (23), and South Korea (14). The survival of the PCB industry in the US is at stake.

Interestingly, when the US government launched the “Chip Act” to bring chip manufacturing back to the US, most people overlooked or even ignored the PCB and chip packaging processes.

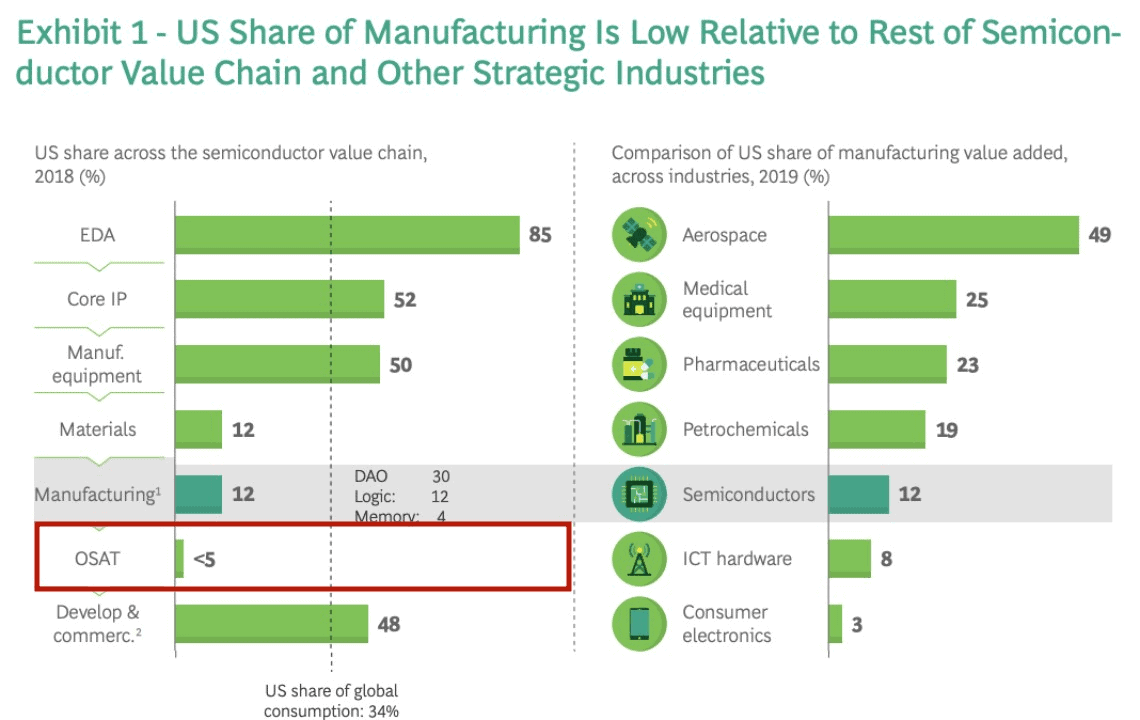

The Semiconductor Industry Association (SIA) has issued two reports advising the US government, namely “Government Incentive Plans and US Semiconductor Manufacturing Competitiveness” and “2020 US Semiconductor Development Overview”. However, if one searches for “packaging” or “PCB” as keywords without considering annotations, there are no search results. Moreover, according to US statistics, the global market share of US outsourced semiconductor assembly and test (OSAT) is significantly lagging behind.

In fact, the importance of chip packaging cannot be overstated. Many industry insiders have pointed out that as Moore’s Law reaches its limits, chip packaging will become the next technology to squeeze out the last bit of potential. With more and more exploration of packaging, Chiplet, for example, has demonstrated the importance of packaging for cost.

The PCB industry, especially the packaging substrates of its segmented tracks, can be said to be the center of the vortex of the US semiconductor self-sufficiency plan.

Furthermore, the PCB industry seems to be quietly reminding the US manufacturing industry. In recent years, there have been constant price increases in PCB materials, and the basic material for PCB manufacturing is CCL (copper-clad laminated board), with copper foil, fiberglass cloth, epoxy resin, and other raw materials as its upstream. The prices of various upstream raw materials for copper-clad laminates have been continuously rising since last year. Taking the low-end price of 35um copper foil as an example, the copper foil price has rebounded by 11.9% from its low point at the end of October last year (with processing fees rebounding by 37.5%). Due to the impact of rising raw material prices, PCB (printed circuit board) companies are strongly expected to raise prices.

In a memorandum, Biden wrote that without actions taken by the President under Section 303 of the Act, it cannot reasonably be expected that the industrial sectors of the United States will timely provide the capacity for the industrial resources, materials, or critical technology projects needed. “I find it necessary to take action to expand domestic production capacity for printed circuit boards and advanced packaging to avoid shortages of industrial resources or critical technology projects that could severely harm our national defense capabilities.”

Given the emphasis on reshoring manufacturing, it seems that the United States has begun to pay attention to the PCB industry.

② Does China need to be concerned about PCB development?

So, does China need to be concerned about the development of PCB? As previously mentioned, the strength of China’s PCB industry is not weak, but the industry is “big but not strong.”

China began PCB development work in 1956. In the 1960s, single-sided circuit boards were mass-produced, small batches of double-sided circuit boards were produced, and research on multilayer PCBs began. In the 1970s, due to the limitations of historical conditions, the development of printed board technology was slow, causing the entire production technology to lag behind advanced foreign levels.

In the 1980s, advanced single-sided PCBs, double-sided circuit boards, and multilayer printed circuit board production lines were introduced from abroad, which improved China’s printed board production technology. In the 1990s, printed board manufacturers from Hong Kong, Taiwan, Japan, and other regions established joint ventures and wholly-owned factories in mainland China, leading to a rapid increase in mainland printed board production and technology.

Local circuit board enterprises emerged across the country like mushrooms after rain, riding the fast train of reform and opening up. In 2006, China surpassed Japan to become the world’s largest PCB production base in terms of output value and the most technologically active country.

China has taken the lead in the PCB market in just ten short years, and one important reason is the high degree of marketization of China’s PCB enterprises.

In addition to brand manufacturers such as Huawei, ODMs make independent decisions on outsourcing circuits and wiring to PCB contract manufacturers, mainly located in Taiwan, which in turn supports the production capabilities of Chinese upstream PCB manufacturers. This cluster formation helps accelerate product launch times, thereby improving production efficiency and delivery capabilities.

Around 2018, it could be considered a period of explosive growth for the domestic PCB industry. With the improvement of the global PCB market, domestic PCB manufacturers also have significant capital advantages. Many leading companies, such as Shennan, Sheng Hong, and Kingboard, have spared no effort in expanding their production capacity. For example, in 2017, Shennan Circuit, which went public, raised RMB 1.268 billion and planned to build the Nantong Shennan Datacom High-Speed High-Density Multi-Layer PCB (Phase I) project.

At the same time, the PCB industry’s mergers and acquisitions market in 2018 set new records in both transaction volume and transaction amount, with multiple M&A cases. For example, Zhongjing Electronics spent RMB 330 million in cash to acquire 55% of Yisheng’s equity and 29.18% of Yuansheng Electronics’ equity. After the acquisition, Zhongjing Electronics held a total of 76.12% of Yuansheng Electronics’ equity; Bomin Electronics proposed to acquire 100% equity of Juntian Hengxun for RMB 1.25 billion.

The development of China’s PCB industry has been rapid, but is it large enough? This raises further questions – how big is big enough?

As of 2019, when China’s manufacturing industry accounted for 20% of the world’s manufacturing industry, then Minister of Industry and Information Technology Miao Wei stated that China had become a world manufacturing power. From the data, China’s PCB industry output value accounts for approximately 53.7% of the global output value, exceeding half of the world’s output value. From this perspective, China’s PCB industry is large enough.

According to statistics from Prismark on the PCB production value in different regions, 47.8% of China’s PCB production value comes from mid to low-end boards. In contrast, the proportion of high-end products such as high-density interconnect (HDI) boards, IC packaging substrates, rigid-flex boards, and metal core boards is only 48.1%, much lower than the 68.6%, 80.4%, and 84.7% in the United States, Japan, and Asia, respectively. Therefore, despite China’s PCB production value being the highest in the world, there is still room for improvement in high-end products.

In terms of end-user demand, the domestic PCB market mainly relies on 4G and 5G base stations, especially in communication equipment where PCB and high-density boards used in servers and data storage account for over 40% of demand. The antennas in 5G base stations are arranged on PCB as a carrier and connection, and the economies of scale have also lowered the cost of PCB.

With a strong market, existing companies, and growing demand, the PCB industry in China is expected to continue to grow.

③ The crisis remains for small and medium-sized PCB enterprises in China

In the development of the market, many PCB companies have fallen along with the tide.

2022 may be a turning point for many small and medium-sized PCB companies. “This year may be the worst year for the PCB industry in the past twenty years.” A company that has been deeply involved in the PCB industry for many years revealed that many factories in the PCB industry were in a state of shutdown in the first half of the year. “It may be worse than 2008 this year.”

In May last year, a PCB factory in Foshan faced a survival crisis due to difficulties in capital turnover, high debt, and the impact of the epidemic, and invited suppliers and creditors to negotiate payment and debt issues. In October, a well-known PCB-listed company, Founder Technology, announced that it had received a “notice” from the Beijing First Intermediate People’s Court because its debt exceeded 1 billion yuan.

In March of this year, a well-known PCB company went bankrupt and restructured. Sichuan Shenbei Circuit Technology Co., Ltd. issued a letter to all creditors stating that the circuit board production and processing industry is facing the dilemma of insufficient domestic demand and a sharp drop in foreign trade orders, and the company is facing serious difficulties. However, our cash flow is almost exhausted and is at a critical juncture of life and death.

The reason for this may be that PCBs used for 5G have new requirements for space and material characteristics. The main raw materials for PCBs are copper-clad boards, semi-cured sheets, copper foils, copper balls, gold salts, inks, dry films, etc. Among these raw materials, copper-clad boards account for about 37% of the cost. Copper-clad boards used for 5G need to meet the requirements of high-frequency and high-speed transmission.

There are relatively few manufacturers that can produce high-frequency and high-speed copper-clad boards, resulting in a high concentration of the industry and stronger bargaining power for downstream PCB manufacturers. The special requirements of 5G for copper-clad boards have caused the overall cost of copper-clad boards to rise, further exacerbating the price increase of copper-clad boards. This cost increase is then transmitted to PCB manufacturers. Small and medium-sized PCB manufacturers with backward production capacity and technology, seeking the market with low-price strategies, have weak bargaining power with customers, and bankruptcy and closure are inevitable due to insufficient funds.

As time develops, the PCB industry will also undergo reshuffling.

Recommended Reading:

- Supercharge PCB Workflows: Modular, Interactive Design

- Enhance Electronics Durability with Heat Management

- SemiKong: The First Open-Source Semiconductor AI Model

- Nvidia and SoftBank: Jensen Huang Meets Masayoshi Son

- How Trump 2024 Election Affects the Semiconductor Sector?

- Facing the Worst in 50 Years: Middle East Silicon Valley

- Shocker: US Chip Titans Slump in Ban Update

- How Much Does One Square Meter of PCB Cost?

- U.S. Launches Ambitious 5-Year Chip Plan: Learn More!

- Tax Storm: Nand Storage Firms in China Under Customs Probe

- Semiconductor Subsidies: The Worst Investment?

- Why Semiconductor CEOs Are Older, Internet CEOs Younger

Disclaimer: This article is created by the original author. The content of the article represents their personal opinions. Our reposting is for sharing and discussion purposes only and does not imply our endorsement or agreement. If you have any objections, please contact us through the provided channels.