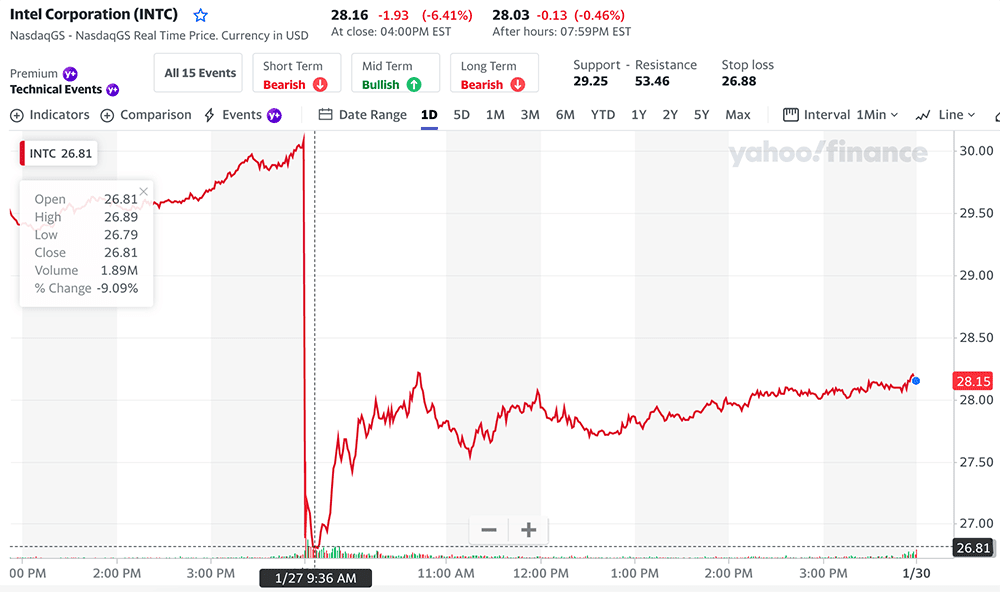

The market value of chipmaker Intel dropped by $8 billion (54 billion yuan) overnight on Jan. 27, 2023, falling to $116.22 billion by the end of the day.

The announcement comes just one day after Intel reported its lowest quarterly revenue since 2016, with $14.04 billion in the fourth quarter of 2022, falling short of market expectations.

“There are no words that can describe or explain Intel’s historic collapse,” said Hans Mosesmann, an analyst at research firm Rosenblatt Securities.

On the same day, Advanced Micro Devices (AMD), Intel’s rival, rose 0.3%.

How did the once-dominant chip industry fall behind? Is the Intel era drawing to a close?

Former king

There should be no dispute that Intel was once the king of the chip industry.

Intel is an IDM semiconductor chip company (From Intel to IDM: Reshaping the Semiconductor Industry) that was founded in 1968 and has a history of more than 50 years. Its core competency is semiconductor R&D and innovation, which includes advanced semiconductor technology, manufacturing capabilities, chip design, and solutions built around the master chip ecosystem.

From 1983, IBM’s personal computer year, to the introduction of Apple’s smartphone and tablet in 2007, Intel dominated the PC market, propelling the US semiconductor industry forward and eclipsing Japanese semiconductor and chip companies.

Intel is the world’s semiconductor technology and chip design leader. Moore’s Law, which has had a profound influence on the development of the industry today, was developed by Gordon Moore, one of the founders of Intel. From the standpoint of industry leadership, Intel and Microsoft’s “Wintel” alliance has dominated and promoted the global PC market since the 1980s.

Intel had become the world’s largest semiconductor supplier as early as 1992. Its development can be divided into several distinct stages:

💡First Stage

In the 1970s, Intel began as a memory company. Intel was able to dominate the design and production of many types of memory as a result of plant expansion and process upgrades, and the business grew significantly.

In 1970, Intel used 12-micron technology to develop the C1103 dynamic random access memory chip, ushering in the era of industrialization of dynamic random access memory chips. Intel created the world’s first processor chip, the Intel 4044, in 1971. In October of that year, Intel successfully listed on NASDAQ, and its share price increased threefold over the next two years. Intel created the first microcomputer in 1972; by 1974, Intel had captured more than 80% of the global RAM memory chip market share, making it the world’s largest memory chip supplier.

💡Second Stage

In the early 1980s, Intel’s main business was dynamic random access memory (DRAM) chips.

However, profits in the US semiconductor industry were declining at the time as Japanese companies became more competitive and aggressively entered the market. Intel was forced to close seven factories, lay off 7,200 workers, and lose nearly $200 million in 1985, its first loss as a public company. If International Business Machines had not stepped in at the height of Intel’s crisis, buying 12% of its bonds to keep its cash flowing, the chip giant might have collapsed or been taken over, reshaping the history of the American information industry.

💡Third Stage

The enormous success of Intel’s microprocessor in the IBM personal computer in 1983 prompted CEO Grove to alter Intel’s business model and basic product direction. Grove decided to shift its focus from the $1 billion-plus memory-chip business to the processor chip market in 1985.

Grove called the decision a “strategic turning point.”

In retrospect, that decision was a watershed moment that propelled Intel out of the memory chip death valley and into 15 years of unprecedented growth. As a result, Intel emerged as the dominant chip company in the personal computer industry, as well as the most profitable semiconductor chip company.

Step down from the altar

For a long time in the history of the industry, Intel (Inside Intel Museum: Silicon Valley’s Tech Revolution) has been the undisputed leader in the market for PC and server processor chips. Many chip titans have left the field one after the other, but AMD, a microprocessor chip company, has been competing with Intel for more than 50 years.

AMD and Intel shared the same Fairchild founders, but AMD had been outsmarted by Intel ever since, with Intel eating meat and AMD eating soup until Su Zifeng, a Chinese-American engineer, joined the team.

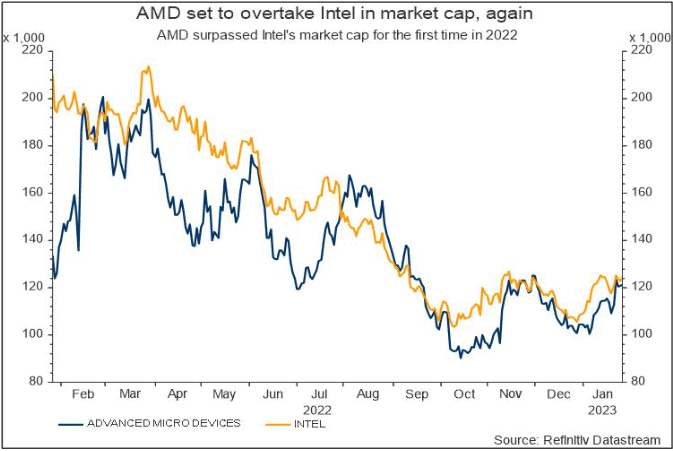

Su Zifeng joined, and the industry was shocked when AMD’s market value surpassed Intel for the first time in history in February 2022, shocking the industry.

AMD is worth more than Intel again after mid-2022, according to Refinitiv’s chart. AMD had a market value of about $121.6 billion at Friday’s close, surpassing Intel by about $5 billion.

Market value is “face”, and revenue is “inside”.

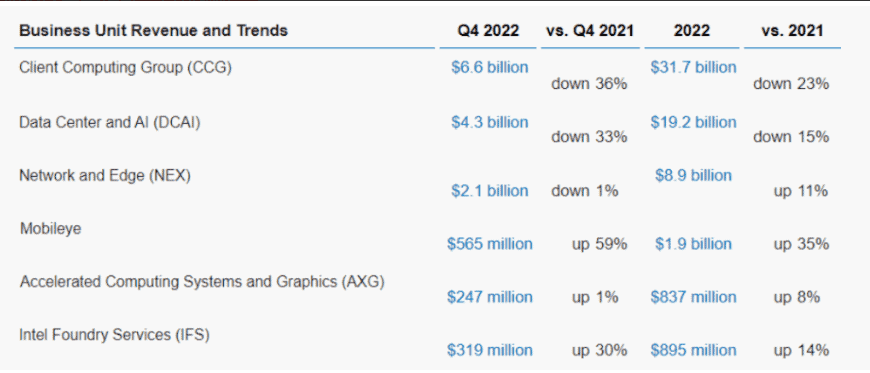

Intel reported revenue of $14 billion in the fourth quarter of 2022, a 32% decrease from the previous year and less than the consensus of $14.49 billion, the lowest quarterly revenue since 2017. Net profit for the full year of 2022 was $8 billion, a direct decrease from $19.9 billion in 2021.

Many analysts believe that Intel will be at a disadvantage in the future, and is expected to lose more market share.

Ignore The Times

“We are prisoners of our own success.”

Former Nokia Chairman and CEO Jorma Ollila once commented on Nokia’s response to new opportunities. The same can be said for Intel.

For decades, the semiconductor industry has followed Moore’s Law. As long as we manufacture in accordance with Moore’s Law, the entire industrial chain will follow the enterprise’s production rhythm. Enterprises can achieve their goal of market control without taking into account external world changes, which also causes Intel to form a closed system.

Since its inception, Intel has been developing, manufacturing, manufacturing, and delivering around Moore’s Law, and it has been successful, but it has also brought them the curse of success: dominance creates closed systems that gradually fail to keep up with the market’s pace of change.

Ignoring the market, on the other hand, will result in severe consequences. Particularly, the times have changed.

Qualcomm, which was developing CDMA phones at the time, wanted to collaborate with Intel in the 1990s, but Intel refused because the market was too small. Later, when Apple attempted to collaborate with Intel on the first iPhone, Intel turned it down for the same reason.

With the success of the iPhone and the release of the Android operating system, the world entered the era of the smartphone explosion. Many mobile phone processor manufacturers, led by Qualcomm, experienced rapid growth. However, when confronted with the burgeoning mobile Internet era, Intel was slow to respond and completely ignored the arrival of a new era.

Intel didn’t announce its entry into smartphone chips until 2012, with its Atom line of X 86 processors. However, due to the high power consumption of the X 86 architecture and compatibility issues with Android applications, major phone manufacturers avoided Intel’s Atom chips. Intel finally gave up after years of struggle.

The second characteristic is its business model. Intel’s business model, dubbed “One package service” for short, is to handle everything from design to manufacturing to packaging.

This model has worked flawlessly in the past, and it is also Intel’s biggest advantage in leading the world for so many years, allowing Intel’s internal links to work seamlessly when launching a product. In fact, many Intel technologies can be performed independently by a variety of companies. However, realizing Intel’s comprehensive expertise from design to manufacturing, ecology, and solutions is extremely difficult.

But the rise of TSMC has changed the rules.

Intel’s semiconductor chipmakers (Intel Unleashes Innovation: Win Laptops Closing in on Mac) were once the most advanced in the world, far ahead of Taiwan Semiconductor and years ahead of AMD. AMD had its own plant in Texas in the beginning, but as the cost of the plant rose and AMD was beaten down by Intel, the semiconductor plant became unviable, and AMD began to become a foundry. But the bad thing turned out to be a blessing in disguise. AMD designed Taiwan Semiconductor Manufacturing, and the two companies collaborated closely to achieve design, architecture, and process breakthroughs.

Intel’s 10-nanometer chips, for example, have been delayed several times, even as rival AMD has moved to 7nm nodes based on TSMC’s foundry technology. AMD’s wildly successful Zen architecture has narrowed the performance gap between the two companies CPUs, particularly since the release of the 7-nanometer Zen2, leading to more players favoring AMD’s processors and the Zen architecture’s Ryzen line of processors beginning to eat into Intel’s share of the PC market.

Taiwan Semiconductor Manufacturing and Samsung Electronics have both introduced 3nm processes, and Intel intends to implement a 3nm equivalent node by the end of 2023.

Intel’s strategy

Intel has gone through several ups and downs since its founding in 1968, from its beginnings as a memory company to its beginnings as a CPU company.

Intel’s current decline will not be reversed in the near future, and competitors will leave little room for him. However, as the world’s most leading and powerful chip giant in the past, and still holding a dominant position in processors with a market share of more than 70%, Intel’s core competitiveness merits careful consideration and debate.

For many years, Intel’s advanced technology and manufacturing have led other companies, and “product performance leadership” has always been Intel’s strategy.

Because the more advanced the process, the smaller the transistors and the lower the power consumption, the more design and innovation can be integrated into the chip and the higher the yield.

How does Intel execute this strategy?

The most important thing is continuous innovation!

Intel has vast resources and releases a new product every cycle (usually a year). When faced with a challenge, it releases chips in a circular fashion, allowing it to release new products every year even if competitors don’t, leaving rivals behind and encouraging consumers to replace their old phones with new ones, resulting in higher profits.

The most well-known example of this occurred in 2002 and 2003, when a company called Transmeta, which manufactured CPUs, attempted to compete with Intel by advertising in Japan that its CPU power consumption was lower than Intel’s. Intel stunned the nation by introducing a low-power chip in just three months. The same is true for AMD. As soon as AMD releases server chips, Intel responds with server chips. Every year, Intel releases new chips for PC processors, regardless of the fortunes of its competitors, keeping them busy while gaining the full support of downstream PC partners.

On the contrary, “product performance leadership” is also a major impediment for Intel. As previously stated, as Moore’s Law progressed, Intel, as the leader in advanced technology, lost its dominance in the manufacturing process and gradually fell behind its competitors Taiwan Semiconductor Manufacturing and Samsung. It is difficult to catch up in a short period of time with the so-called slow step by slow step.

Words in the End

The industry was shaken by Intel’s latest dismal earnings forecast, which highlighted the challenge of weak post-pandemic PC demand.

Of course, Intel itself knows it can’t continue to thrive solely on PCS.

In recent years, Intel has shifted away from the PC market and toward a data-centric one. To that end, the company has established six technological pillars, which include process and packaging, architecture, memory and storage, interconnection, security, and software. Intel’s next 10 years and the next 50 years will be defined by exponential innovation based on six technical pillars.

To achieve value, technological innovation must be implemented in application scenarios. Intel has also laid the groundwork for artificial intelligence, autonomous driving, and other fields in this regard. It’s worth noting that Intel’s autonomous driving unit, Mobileye, performed admirably in its most recent earnings report. It went public in December and reported adjusted earnings per share of 27 cents. Revenue increased 59% to $656 million, and revenue growth for Mobileye is expected to be strong in 2023. $2.19 billion to $2.28 billion.

In fact, not only Intel, AMD, Nvidia, and other chip companies have been harmed by this industry winter; Intel’s situation reflects the industry’s current state. Despite its current passive position, Intel is thought to have a good chance of turning things around. It will be able to innovate its way back to the top if it makes the right moves to break free from the comfort zone it has created through patent barriers.

Recommended Reading:

- Intel Rejects Warranty Over i9 14900K Liquid Metal Damage

- Upgrade Your PC: Best Value CPUs in October 2023

- Facing the Worst in 50 Years: Middle East Silicon Valley

- Intel vs Arm: The Future of PC Processors

- Intel CEO Gelsinger: Intel has three major failures!

- Windows Moves Away: Intel Crisis Rocks Wintel Alliance

- Intel’s 2024 Graphics: Battlemage Architecture Unveiled

- Massive $3.2B Israeli Investment Fuels Intel Chip Plant

- Intel vs AMD: The Battle for Microsoft’s Custom SoC Business

- AMD vs Intel 2024: Epic Tech Showdown Heats Up

- Intel Unveils 2024 CPUs: Ultra-Low Power, No Hyper-Threading

- Intel Xeon LGA 7529: Quadruple the Size of LGA 1700!

- Top 5 Intel CPUs Ever: Unmatched Performance & Speed

- Ancient Tomb Halts Intel German Chip Factory Build

- Intel Crisis: Unstable Gaming on 13th & 14th Gen CPUs!

- Intel in Russia: 2023 Revenue Hits Zero – Details!

- Intel 14A Process Vital for Post-2025 Dominance